The Freeze Was Real. It's Melting. The Debate Hasn't Caught Up.

There’s a fight going on among housing people right now, and both sides are half-right in a way that makes the whole conversation useless.

One camp says we have a supply problem — build more houses. The other says no, we have an affordability problem: millions of homes are “locked up” by owners sitting on 3% mortgages who won’t sell into 7% rates, so the shortage is a mirage.

The argument misses the one thing the data makes obvious: both camps are describing different years of the same market.

How to read this

This report leans on national for-sale listing flow and absorption from the ZoneVista warehouse (mv_inventory_trends, 924 metros, snapshot 2026-04-30), cross-referenced against a supply-signal-by-affordability cross-tab across 389 metros. National series are built from summed metro counts, with ratios rebuilt from those sums rather than averaged across metros — so big markets carry their real weight and small-market noise doesn’t distort the aggregate.

One honest limit up front, because it’s load-bearing: the warehouse cannot see locked mortgages directly. There is no national registry of who holds a cheap rate. What it can see is the fingerprint a freeze leaves behind — new listings drying up while demand cools at the same time. Everything below is that fingerprint, not the thing itself.

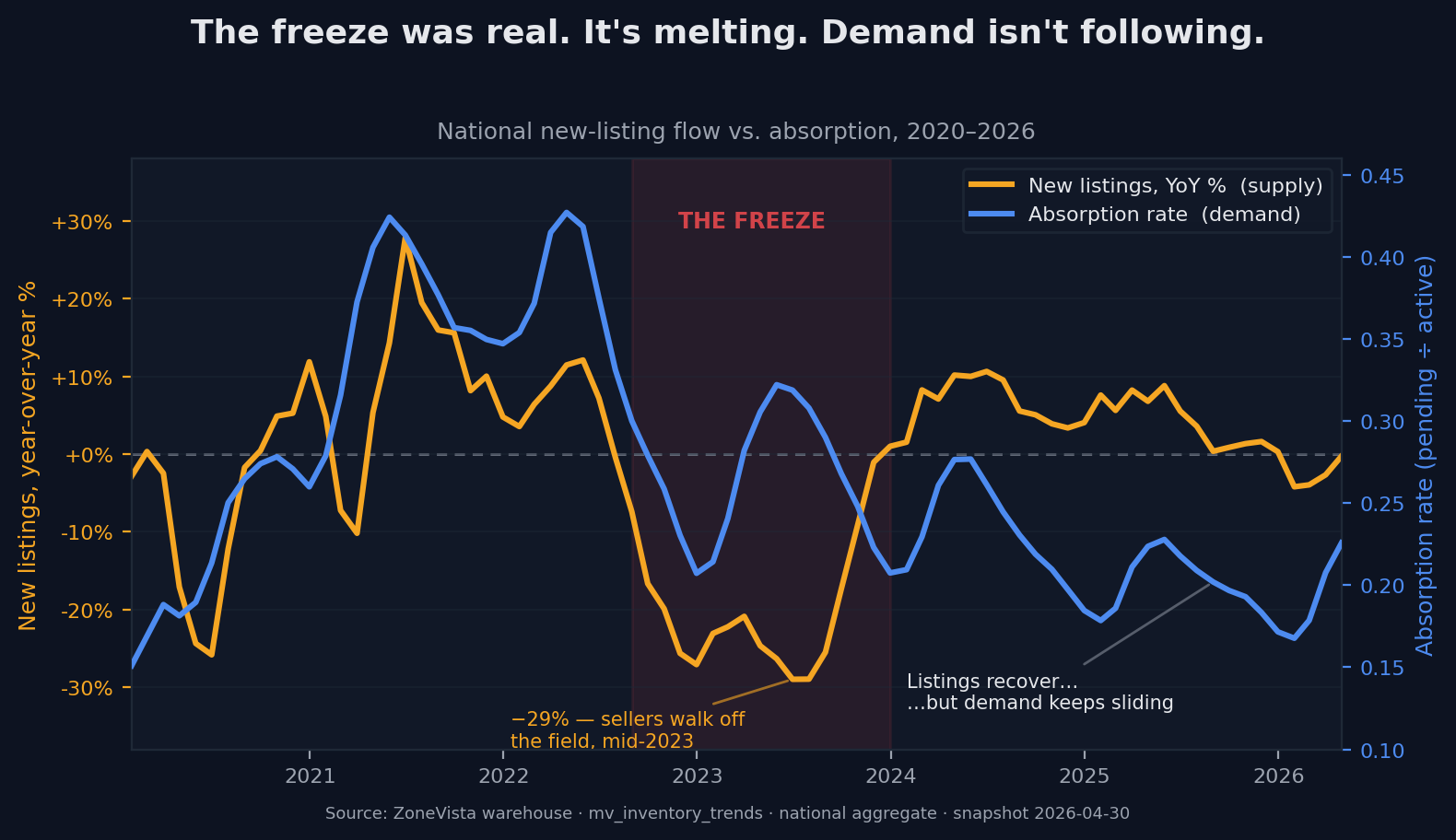

The freeze was real (2022–2023)

New for-sale listings went negative year-over-year in August 2022 and stayed negative for seventeen straight months, bottoming near −29% in mid-2023.

The direction of absorption is what settles the supply-vs-shortage question. If a genuine shortage were eating supply, buyers would be absorbing everything in sight — absorption would spike. Instead, absorption fell right alongside listings. That is not demand outrunning supply. That is sellers walking off the field. On the question of 2022–23, the lock-in camp was correct.

The constraint already moved (2024–2026)

Active inventory has since rebuilt from a frenzy-era trough of roughly 660,000 listings back above 1.1 million — and absorption kept sliding the entire way, down to one of the weakest readings in years.

Read those two facts together. Inventory is coming back. Buyers still aren’t biting. The freeze is thawing, and what’s replacing it isn’t a supply shortage — it’s a demand ceiling. The constraint migrated from the supply side to the demand side, and it did so roughly a year ago.

Affordability isn’t where the tightness is

Here is the part neither camp says out loud. If unaffordability were caused by tight supply, the least-affordable metros would cluster in the tightest markets. They don’t.

Across 389 metros at the latest snapshot, the share of metros flagged least-affordable is actually higher in balanced-supply markets (29%) than in tight ones (24%), with the tightest band landing almost exactly where pure statistical independence would put it. Supply tightness has essentially no power to explain whether a metro is unaffordable. You cannot draw the affordability map from the supply map. They are nearly orthogonal.

The expensive metros are a split decision

The high-cost job-center metros everyone calls locked don’t read as one thing. San Francisco, San Jose, and Boston are still genuinely supply-tight. Seattle, Los Angeles, and San Diego are restocking fast — Seattle’s active inventory is up roughly 26% year-over-year. The loose end of the price spectrum is almost entirely resort and second-home markets, which are loose for reasons that have nothing to do with the lock-in debate.

There is no single national supply verdict for expensive metros. There’s a transition, and it’s uneven.

What to do with this

Stop arguing supply versus affordability as if they’re the same axis pointing opposite directions. They aren’t. Ask which one is actually binding in your market, this quarter. For much of the country, the answer flipped about a year ago — and the people still fighting the last war haven’t noticed the ground move under them.